Parting ways with a car is always a little bittersweet. Whether you’ve sold it on to another driver, traded it at a dealership, or watched it head off on the back of a recovery truck to the scrapyard, there’s more to the process than simply handing over the keys. Cars carry responsibilities, and if those loose ends aren’t tied up properly, it can cost you more than you expect.

The most common mistakes? Forgetting to deal with the tax and insurance. Many drivers assume the sale itself makes everything stop automatically, but that’s not the case. Car tax refunds are now automatic through the DVLA, but your insurer won’t lift a finger unless you make the call. And when you forget, the payments keep leaving your bank account, sometimes for months.

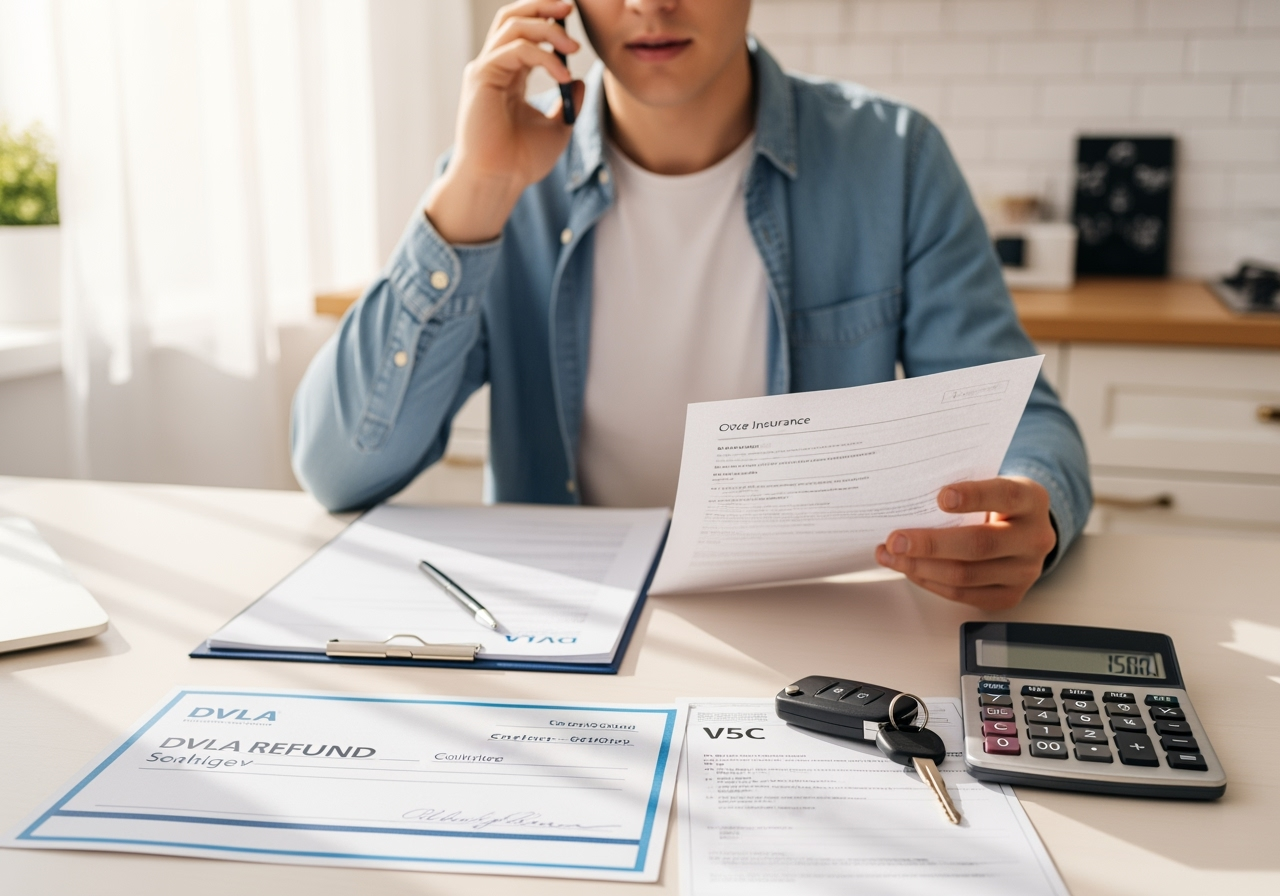

This guide takes you through every step of how to cancel car tax after selling and how to cancel car insurance after selling or scrapping. Think of it as a neighbourly chat over the fence from an old mechanic who’s seen it all before, from customers forgetting refunds to insurers quietly taking cash long after the car’s gone. By the time you’re finished here, you’ll know exactly what to do, when to do it, and how to avoid the common traps.

Understanding why tax and insurance matter after a sale

Car ownership is tied to more than just the V5C logbook. Two obligations run alongside your car until the day you stop being the registered keeper: vehicle tax and insurance.

- Car tax keeps your vehicle legally on the road. Without it, you risk penalties from the DVLA.

- Insurance protects you, your passengers, and other road users. Even a short lapse can cause legal trouble.

When you sell or scrap your car, those obligations don’t vanish automatically. The DVLA takes care of tax once you notify them, but insurance stays active until you tell your provider otherwise. Understanding the difference saves you from paying money for nothing.

Car tax refunds: what happens automatically

The good news first: the DVLA made life much easier with an automated tax refund system.

Here’s how it works:

- As soon as you notify the DVLA that your car is sold, transferred, or scrapped, the tax is automatically cancelled.

- You’ll receive a refund for any complete months of unused tax. Sell or scrap mid-month, and you lose the rest of that month.

- Refunds are sent by cheque to the address on your V5C logbook. Direct transfers aren’t offered.

- Refunds usually arrive within 4–6 weeks.

That means you no longer need to physically “cancel” road tax. Once the DVLA knows you’re no longer the keeper, they stop the tax automatically.

Key Takeaways

- Cancel car tax after selling isn’t a manual task anymore; DVLA does it automatically.

- Refunds arrive by cheque.

- Make sure your V5C logbook address is correct to avoid delays.

What if the tax refund doesn’t arrive?

Every system has its snags, and the DVLA’s refund process is no different. Missing refunds usually happen for one reason: paperwork errors.

Picture this: A customer I knew years back sold his Mondeo just before moving house. He dutifully sent the V5C to the DVLA but forgot to update his address first. The refund cheque went to his old address, and by the time he realised, someone else had already cashed it. It took him months of calls and stress to put right.

If you’ve waited more than six weeks for your refund:

- Check your address on the logbook. If it’s outdated, that’s likely the problem.

- Contact the DVLA by phone or through their website.

- Keep your registration number and V5C details handy before calling.

Key Takeaways

- Refund delays are usually caused by incorrect addresses.

- Always update your V5C before selling.

- Contact the DVLA if the refund doesn’t show after six weeks.

For peace of mind, you can also read our guide on the documents needed to scrap a car, which covers how DVLA notifications work in more detail.

Cancelling your car insurance: why you can’t skip it

Unlike tax, insurers won’t act unless you do. If you don’t tell them, the direct debits continue.

Think of insurance like a broadband contract. The provider won’t know you’ve moved unless you call, so the bills keep arriving. Car insurance is no different; unless you cancel, you’ll keep paying for cover you no longer need.

That’s why it’s vital to cancel car insurance after selling or scrapping. Even if the car is gone, your provider assumes the risk still exists until you confirm otherwise.

Key Takeaways

- Insurance does not cancel automatically.

- Always contact your insurer directly.

- Failing to cancel wastes money and can create complications.

The right time to cancel insurance

Cancelling too soon or too late can both cause problems. The trick is to act the moment ownership changes hands.

- Private sale: Cancel as soon as the V5C is signed over.

- Part-exchange: Wait until the dealer confirms the car is in their name.

- Scrap collection: Cancel once the recovery truck has taken the vehicle away.

I knew a driver who scrapped his car but didn’t bother cancelling his policy until months later. By then, he’d paid nearly £100 unnecessarily.

Key Takeaways

- Cancel at the exact moment ownership changes.

- Don’t leave it weeks after the sale.

- Always ask for confirmation from your insurer.

How to cancel your insurance policy

Most insurers offer three routes:

- Phone call – The fastest and most reliable. You speak to an advisor, confirm cancellation, and ask about fees.

- Online portal – Some insurers provide digital cancellation options. Useful, but not universal.

- Letter – Still accepted, but painfully slow and prone to error.

Even today, the safest method is by phone. It gives you peace of mind and allows you to check for any remaining charges or refunds.

Key Takeaways

- Phone is the quickest route.

- Online works if your provider supports it.

- Letters are outdated and risky.

What you’ll need before calling your insurer

Being prepared makes the call smoother. Insurers will usually ask for:

- Policy number.

- Date of sale or scrap.

- Buyer’s details, if applicable.

- Bank details for refunds.

It’s much easier to have these ready than to fumble around while you’re on hold.

Key Takeaways

- Keep your policy number handy.

- Provide the sale/scrap date.

- Have bank details ready for refunds.

Can you get a refund on your insurance?

In many cases, yes. If you cancel partway through the year, insurers usually refund the unused portion of your premium. But there are caveats:

- Fees apply. Most insurers charge £25–£60 for mid-term cancellations.

- Claims block refunds. If you’ve made a claim during the policy, don’t expect money back.

- Minimum premiums. Some insurers set non-refundable minimum amounts.

I once dealt with a young driver who cancelled his Fiesta’s insurance after scrapping it. He expected a tidy refund but had made a windscreen claim months earlier. Result: no refund at all.

Key Takeaways

- Refunds depend on unused months left.

- Fees often reduce the amount you get back.

- Claims usually mean no refund.

Things to check before cancelling

It’s not just about your own payments. Two other checks matter:

- Buyer’s insurance – Never let the new keeper drive away uninsured. You could both face penalties.

- Your replacement cover – If you’re switching cars, sort new insurance before cancelling the old one.

A man I knew once cancelled his old policy before insuring his replacement car. He drove it home uninsured, was stopped by the police within an hour, and ended up with a fine, points, and higher premiums for years afterwards.

Key Takeaways

- Confirm the new owner has cover.

- Avoid any gap in your own policy.

- Driving uninsured is a serious offence.

Regional notes: big city considerations

Selling in Manchester

If you’re planning to sell your car in Manchester, get tax and insurance sorted quickly. Busy city roads mean more police checks, and mistakes are rarely overlooked.

Selling in London

When you sell your car in London, strict emissions regulations make correct paperwork vital. Cancel insurance promptly to avoid unnecessary costs.

Selling in Birmingham

Looking to sell your car in Birmingham? Clean Air Zone rules mean scrap yards often work directly with the DVLA, but insurers won’t act without your call.

Final checklist: the steps you must take

- Notify the DVLA that your car has been sold or scrapped.

- Wait for your automatic car tax refund.

- Contact your insurer to cancel car insurance after selling.

- Check for refunds from both DVLA and your insurer.

- Update your V5C logbook address before selling.

- Make sure there are no gaps in cover for your next car.

- If scrapping, get a quote to scrap your car through our network.

- If selling, find out how to sell your car securely and at fair value.

- For guidance at any point, contact us.

Analogy: Insurance as a subscription

Think of insurance as a subscription service, like streaming TV. Cancel late, and you’ve paid for a month you never used. Forget entirely, and the bills keep coming even though you’ve got nothing to watch. Insurance works exactly the same way; unless you tell them to stop, it carries on.

Anecdote: The customer who forgot

Back when I ran my small garage, I had a lad come in proud as punch that he’d finally sold his old hatchback. He thought the sale meant everything was handled. A month later, he came back complaining about another insurance payment leaving his bank. He hadn’t called his provider, and it cost him nearly £70 for nothing. It was a reminder I’ve passed on to customers ever since: insurers won’t act unless you do.